Mortgage renewal season in 2026 is shaping up to be one of the most financially stressful moments many Canadian homeowners have faced in decades. Millions of households who locked into ultra-low rates in 2021 are now approaching renewal at rates that are meaningfully higher, even after recent stabilization.

For many people, this will not just be a paperwork exercise. A rushed decision, blind acceptance of a lender’s offer, or misunderstanding of renewal options could translate into thousands of dollars in extra interest over the next five years.

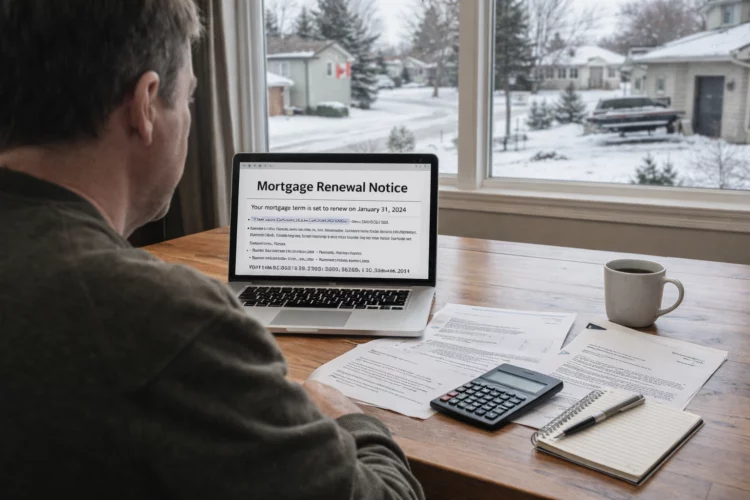

Here is a clear, practical guide to what is happening in the mortgage market, what renewals really mean, and how homeowners can avoid locking themselves into years of unnecessary costs.

Why 2026 Is a Critical Year for Mortgage Renewals

A large wave of Canadian mortgages is coming due, and timing could not be more sensitive.

How Many Mortgages Are Up for Renewal

Roughly 1.2 million Canadian mortgages are expected to renew across 2025 and 2026. Many of these loans were signed in 2021, when five-year fixed rates were near historic lows.

For borrowers, the gap between old rates and renewal offers can feel like a shock, even if rates have stopped climbing.

Why This Renewal Cycle Feels Different

In past cycles, rate changes were often gradual. This time, borrowers are moving from emergency-level rates to a more normal interest rate environment in a short span of time. That adjustment is forcing tough budget conversations for many households.

The Mortgage Rate Outlook for 2026

One of the biggest questions homeowners ask is whether rates will rise, fall, or stay flat.

Where Interest Rates Stand Right Now

As of early 2026, the Bank of Canada has held its policy rate at 2.25 percent for several months. That decision has brought a period of relative stability after a long stretch of increases.

Because of this pause, prime lending rates in Canada have also remained steady, sitting around the mid four percent range.

What This Means for Different Borrowers

Fixed-rate mortgage holders will not see changes until renewal, regardless of what happens with policy rates in the meantime.

Variable-rate mortgage holders are less likely to experience short-term payment increases while rates remain on hold. If cuts eventually arrive later in 2026, variable rates are typically the first to move down.

Why No One Can Promise Rate Cuts

While inflation has eased closer to target levels, global trade risks and economic uncertainty remain. That means homeowners should plan based on today’s reality, not hope for future cuts.

What a Mortgage Renewal Actually Is

Mortgage renewal is often misunderstood, especially by first-time homeowners.

Renewal Versus Paying Off Your Mortgage

At the end of a mortgage term, usually every five years in Canada, you are not required to repay your entire mortgage balance. Instead, you agree to a new term, rate, and conditions for the remaining balance.

That process is known as renewal.

Your Two Main Choices at Renewal

You can renew with your existing lender, often with minimal paperwork.

You can switch to a new lender and negotiate a new mortgage contract.

Both options come with advantages and risks, depending on your situation.

Why Automatically Renewing Can Be Costly

Many lenders offer automatic renewals if borrowers do not respond to renewal letters.

The Convenience Trap

Automatic renewal can reduce stress, but convenience often comes at a cost. Renewal offers are not always competitive, and the terms may be less flexible than what other lenders are willing to offer.

Once renewed, breaking the mortgage early can trigger penalties, especially on fixed-rate terms.

Why Shopping Around Still Matters

Even a small difference in interest rate can translate into thousands of dollars over a five-year term. Spending time comparing options before renewal can deliver meaningful long-term savings.

Tip One: Start the Renewal Process Early

Preparation is one of the most powerful tools homeowners have.

When to Begin

Ideally, start reviewing your mortgage options several months before your renewal date. Proposed industry changes may extend renewal notices to four to six months, but borrowers should not wait for paperwork to arrive.

What to Do First

Request a renewal offer from your current lender.

Gather quotes from other lenders or speak with an independent mortgage broker.

Compare not only interest rates but also penalties, payment flexibility, and prepayment privileges.

Tip Two: Look Beyond the Interest Rate

The lowest rate is not always the best deal.

Why Flexibility Can Save You Money

Life changes happen. Job changes, relocations, family growth, or unexpected expenses can all force a change in housing plans.

Mortgage features like portability, shorter terms, and generous prepayment options can protect you from costly penalties if your plans shift.

Fixed Versus Variable Is Not Just About Rates

If you think you may sell or move before the end of your term, locking into a long fixed-rate mortgage could be expensive. In those cases, shorter terms or variable options may provide more flexibility.

Tip Three: Revisit Your Amortization Strategy

Renewal often allows you to reset your amortization period.

Longer Amortization

Lower monthly payments.

Higher total interest over time.

Useful for short-term cash flow relief.

Shorter Amortization

Higher monthly payments.

Lower total interest paid.

Faster progress toward owning your home outright.

This decision should reflect both current financial pressure and long-term goals.

Tip Four: Stress Test Rules Have Changed

Recent policy changes have altered the renewal landscape.

What Changed for Renewals

Borrowers switching lenders at renewal are no longer required to requalify under the mortgage stress test, provided they are not increasing the loan amount.

Why This Matters

This change increases competition among lenders and gives borrowers more negotiating power. It makes switching lenders more realistic for homeowners who might otherwise be trapped by stricter qualification rules.

Can a Mortgage Renewal Be Denied

In most cases, renewals are approved automatically, but denial is possible.

Situations Where Denial Can Happen

Severe changes in income.

Repeated missed payments.

Major deterioration in financial stability.

What to Do If It Happens

Options include renegotiating with the same lender, switching lenders, or working with an independent mortgage broker to explore alternative solutions. Credit unions and smaller lenders can sometimes offer better terms than large banks.

Is It Ever Smart to Renew Early

Early renewal can make sense, but only after careful math.

When Early Renewal Helps

If the new rate is meaningfully lower than your current rate.

If penalties are low enough to justify the switch.

If budget certainty is more important than potential future savings.

What to Calculate First

Ask your lender about penalties for breaking your current mortgage. Compare those costs against projected savings under the new rate.

Renewal Versus Refinancing: Not the Same Thing

Renewal keeps your loan balance the same.

Refinancing creates a new, larger loan by tapping into home equity.

When Refinancing Makes Sense

To fund renovations.

To consolidate high-interest debt.

To improve monthly cash flow.

Refinancing involves requalification and should be evaluated carefully, especially in a higher-rate environment.

The Bottom Line for Canadian Homeowners in 2026

Mortgage renewals in 2026 are not just administrative milestones. They are financial turning points. Accepting the first offer without comparison, ignoring flexibility, or misunderstanding renewal options can lock households into higher costs for years.

Rates may remain stable in the near term, but certainty is never guaranteed. Homeowners who prepare early, understand their options, and negotiate from a position of knowledge stand the best chance of protecting their budgets and long-term financial health.

In a year when millions of mortgages reset, the smartest move is not guessing where rates will go. It is making a renewal decision that still works if life, and the economy, does not go exactly as planned.